Blockchain Technology Advantages and Disadvantages

Blockchain technology is important in many fields, offering improved security and transparency in transactions. This article will discuss both – blockchain technology advantages and disadvantages.

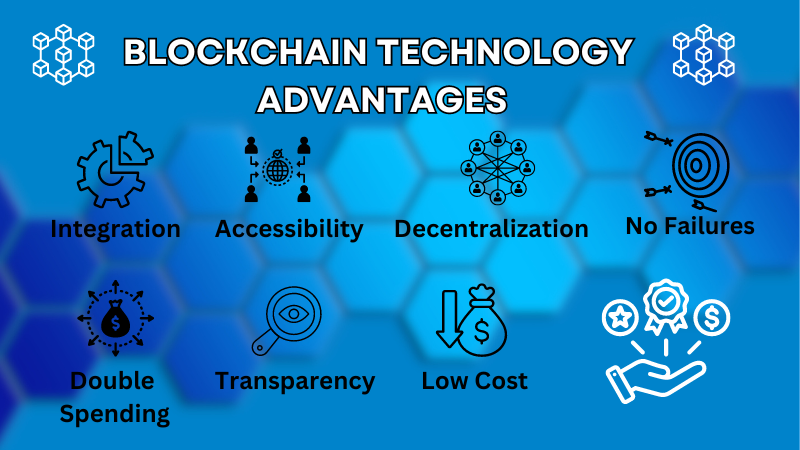

Blockchain Technology Advantages

Blockchain technology is the basis on which cryptocurrencies operate, making it possible to trade cryptocurrencies in a decentralized and secure way. You can read more about the best crypto trading strategies.

Integration

Current systems can incorporate blockchain technology in two primary ways: as a platform for applications or as Blockchain-as-a-Service.

A platform for apps lets people use decentralized technology to create and launch blockchain-based applications. You can track and confirm different kinds of data with these applications, like money transfers, supply chain details, or identity records.

Applying a platform application could be an adaptable and economical method to make use of the advantages that come with blockchain technology.

Alternatively, Blockchain-as-a-service (BaaS) allows companies to link straight with blockchain networks and utilize them for creating and launching applications.

BaaS suppliers present various services such as infrastructure, assistance, and advisory to aid firms in applying and utilizing blockchain technology.

BaaS is very helpful for companies that wish to utilize blockchain but lack the resources or knowledge to create and manage their infrastructure.

Double Spending

Double spending happens when someone uses the same digital money twice as if they are cheating. Blockchain is a record book everyone can see that keeps and checks transaction details with secret codes.

When someone does a deal on the blockchain, it gets saved in a shared database and most of the network’s computers check it using codes. This makes a record that nobody can change and everyone can follow, which helps to make sure deals are right later on.

A consensus algorithm, which is for confirming transactions, stops someone from spending the same money twice. A transaction needs more than half of the network’s nodes to agree on it before we can trust that it’s real.

It makes sure only real deals go on the blockchain and stops people from trying to use the same digital thing twice. A shared record book, secret codes for checking, and a way everyone agrees help stop double spending in a blockchain.

Accessibility

Suppose you have a computer and can connect to the internet. In that case, you can participate in a public blockchain network as it is not controlled by any single group, and it welcomes everybody.

In usual central systems, people usually cannot control their data themselves and they might be at risk because bad people could misuse it.

However in a blockchain network that works with peer-to-peer connections, the users get more power to manage their information since they can decide what details to share and who they want to share it with.

Blockchain technology offers strong security and clear visibility which helps ensure that people manage their details themselves, preventing misuse by anyone else. Giving individuals greater power over their data stands out as a major benefit of using blockchain.

Transparency

A public ledger records blockchain transactions for all internet users to see. It shows the amount of funds in each wallet while keeping the owner’s identity unknown. An individual or a collective can link to a wallet. The clear benefit of blockchain is that it keeps things visible while also keeping enough privacy.

Blockchain technology has a feature where once data is put on the ledger, it cannot be altered or removed. This happens using cryptography like hashing that gives every data block a special identifier.

If someone tries to modify the information within a block, it would lead to a new hash identifier showing other participants the data was changed.

Moreover, everyone involved can usually view the ledger system on a blockchain, increasing how clear and open the stored data is on this network.

Decentralization

A blockchain enables people to send value directly to each other without the need for a middleman or central power. Many servers across multiple locations store the information, and everyone involved confirms it through agreement.

Due to this, those who make transactions do not need to know each other personally; they can still exchange in an environment where trust is not required.

When you think about good and bad sides of blockchain technology, a plus point is it takes away the requirement for go-betweens in a process. This is helpful as these middle people usually ask for money to help with their work, and this expense can grow if there are many steps in that process.

Also, it is not certain that intermediaries will always act with honesty and openness in their transactions. They might participate in dishonest activities for their own gain, harming other people.

If we remove these go-betweens using blockchain technology, it could make the system more trustworthy by taking away this possible cause of corruption.

Low Cost – One of the Blockchain Technology Advantages

Because blockchain removes the necessity for central servers to manage activities, it reduces the extra expenses.

Transactions occur straight on a blockchain without any middlemen or central authority, so there are no banking or payment handling fees. The agreements and dealings are included in the system, often not needing work from people.

This makes it possible for people to pay less money in transaction costs. Usually, when someone uses the normal ways, they have to give extra money for these services. If there are many steps in a process, these extra charges can become more with time.

On the other hand, blockchain technology might provide smaller fees and faster transactions for simple money transfers and person-to-person payments. It is necessary to point out that the particular costs linked with employing blockchain technology can differ based on the exact way it is used in a blockchain network.

No Failures

As a spread-out network, blockchain has strong security and removes the chance of just one place failing. If a hacker gets into the main server or database, they can quickly ruin your company’s whole network, but this is not true with blockchain.

When every node shares the database, it makes the network very safe and protects it from being tampered with. That’s because a blockchain is like a book that everyone can write together – it keeps data and has rules for agreeing on what information is true before putting it into the book.

It’s hard for someone to put wrong or fake information into the blockchain, which really lowers mistakes and cheating.

Also, because there is a system where everyone agrees on the data and we don’t have to enter it by hand, this lessens human mistakes even more and makes the blockchain’s information very trustworthy.

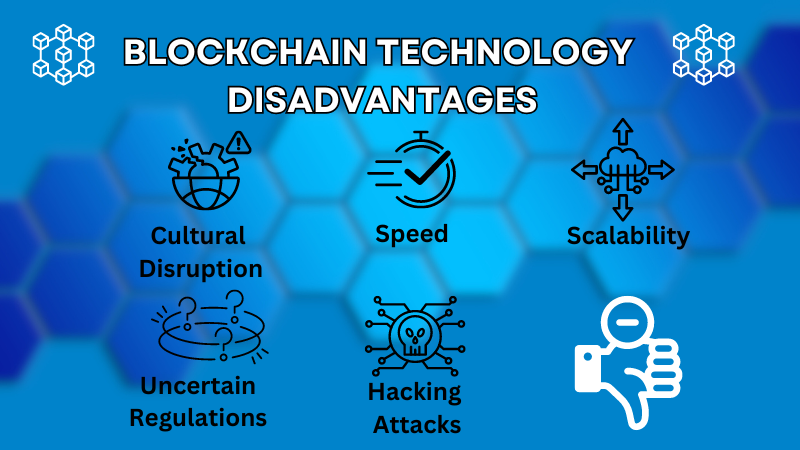

Disadvantages of Blockchain Technology

Cultural Disruption

A possible downside of utilizing blockchain technology might be its capacity to unsettle traditional business models and cultural ways. This happens as blockchain can deeply alter the functioning of systems and sectors, posing difficulties for entities accustomed to long-standing conventional approaches in adjusting to new shifts.

In some situations, using blockchain technology could make some markets and industry sectors become outdated because it changes how companies work and communicate with each other.

Organizations should thoughtfully weigh up the advantages and disadvantages of blockchain for their business ways and activities before they choose to implement it.

Uncertain Regulations

Regulations that are not clear can be a big problem or something that makes people less likely to use blockchain technology. This situation with no strict rules can also help increase the issue of ICO scams, where people or groups get money by selling tokens that might have no real worth.

Additionally, the absence of regulatory measures in the cryptocurrency space may cause challenges for government bodies and big companies to quickly implement blockchain technology. They might be reluctant to embrace a system without similar supervision as found with other financial technologies.

Speed – One of Blockchain Technology Disadvantages

Blockchain technology’s speed has a connection with its scalability issue, which is also a significant downside. Blockchains are becoming more popular for straightforward peer-to-peer payments and international fund transfers because they have low costs and settle immediately.

But when it comes to complicated transactions in supply chains or managing identities, these processes can take more time than older technologies would need.

Blockchain systems such as Bitcoin and Ethereum have a limit of 20 transactions per second, while traditional platforms like Visa and Nasdaq can handle up to 5000 transactions in the same time frame.

The gaming sector, which deals with countless small-scale transactions every moment, requires technology that can manage many more operations quickly.

Blockchain transactions might not happen as quickly compared to other methods because the computation demands of blockchain technology often require more repetition than centralized servers do.

Whenever the ledger gets a new update, all or maybe some of the network’s nodes have to refresh their own ledger copy too. This step is important since every node in this type of system must keep its own version of the record book.

However, it might make processing transactions take longer as well. Newer blockchains like Shardeum is aiming to scale limitlessly through innovative protocols.

Hacking Attacks

Even though we have discussed how blockchain improves the protection of our records and belongings, it is important to remember that this technology and its industry are still at a beginning stage.

For clarification, our discussion does not concern isolated blockchains such as L1 platforms. Layer 1 blockchains are known for their strong protection against security issues.

To simplify it, L1 blockchains such as Shardeum and Ethereum can be seen as the operating systems in the Web2 era, which different applications use to provide helpful products and services to users.

Solutions made to work with L1 blockchains, for example, the bridges that let you exchange and move tokens between different chains, usually do not offer the same strong security through consensus algorithms that L1 blockchains are famous for.

What is more concerning is that these solutions often have less decentralization which can make them open to harmful actions on a public network. Classic rug pulls exist in the world of traditional finance as well as in Web3.

These scams happen when developers behind a cryptocurrency project or mutual fund decide to leave the project and take all the money that investors put into it.

When you observe these patterns, they resemble the internet era of the late 1990s and early 2000s. During that time, news about malware, antivirus programs, phishing attempts, and various cybercrimes seemed constant.

Essentially, any fresh system or protocol will always be vulnerable to malicious individuals exploiting them with the intent of stealing money or causing different kinds of harm.

Scalability

Scalability might be the biggest downside of blockchain technology because it struggles to manage many transactions at once. Blockchain processes fewer transactions each second since most nodes must confirm every transaction before adding it to a block. This leads to issues like network congestion and high transaction costs.

Another problem with blockchain technology is that it sometimes does not work well with older networks.

This can be a big issue for companies that depend on these existing systems. There are situations where you might have to change the old network completely if you want to start using blockchain, and this requires a lot of effort.

People or organizations may doubt this change or be against it. Overall, when thinking about using this technology, it’s important to remember that combining blockchain with older networks can be a challenging thing.

Conclusion of Blockchain Technology Advantages and Disadvantages

Blockchain technology has many benefits, such as better security, clear transactions, and no need for middlemen, making things more efficient.

However, it also faces challenges like handling large amounts of transactions at once, uncertain rules, and security risks.

As blockchain grows, these strengths and challenges will influence how different industries and people use it.

Frequently Asked Questions – Blockchain Technology Advantages and Disadvantages

What is blockchain technology❓

Blockchain technology is a decentralized digital ledger system that records transactions across multiple computers in a secure and transparent manner. It forms a chain of blocks, each containing a unique record of transactions.

How does blockchain ensure security❓

Blockchain employs cryptographic techniques to secure transactions and data. Each block is cryptographically linked to the previous one, making it difficult to alter or tamper with the data. Additionally, the decentralized nature of blockchain reduces the risk of a single point of failure.

What are the advantages of blockchain technology❓

Some advantages of blockchain technology include decentralization, enhanced security, transparency, immutability, and efficiency. It eliminates the need for intermediaries, promotes trust among participants, and streamlines processes through features like smart contracts.

Can blockchain be used beyond cryptocurrencies❓

Yes, blockchain technology has applications beyond cryptocurrencies. It can be used in various industries such as finance, healthcare, supply chain management, and identity verification to improve efficiency, security, and transparency.

What are the disadvantages of blockchain technology❓

Some disadvantages of blockchain technology include scalability issues, energy consumption, regulatory uncertainty, privacy concerns, and a lack of interoperability between different blockchain networks.

How does blockchain ensure transparency❓

Blockchain ensures transparency by recording all transactions on a public ledger that is visible to all network participants. This promotes accountability and trust as participants can independently verify the integrity of transactions.